Source: Montag & Caldwell, FactSet.

PVT=Present Value Total; P/PVT=Price to Present Value Total and represents our estimate for the S&P 500’s price relative to our estimate of its intrinsic value. ERP stands for equity risk premium. ERP is calculated by subtracting the 10 year Treasury Yield from the earnings yield for the S&P 500. ERP is the additional return that investors would expect to earn by investing in the stock market over a risk-free asset. This premium compensates investors for the higher risk of investing in stocks. Monthly data as of May 31, 2024

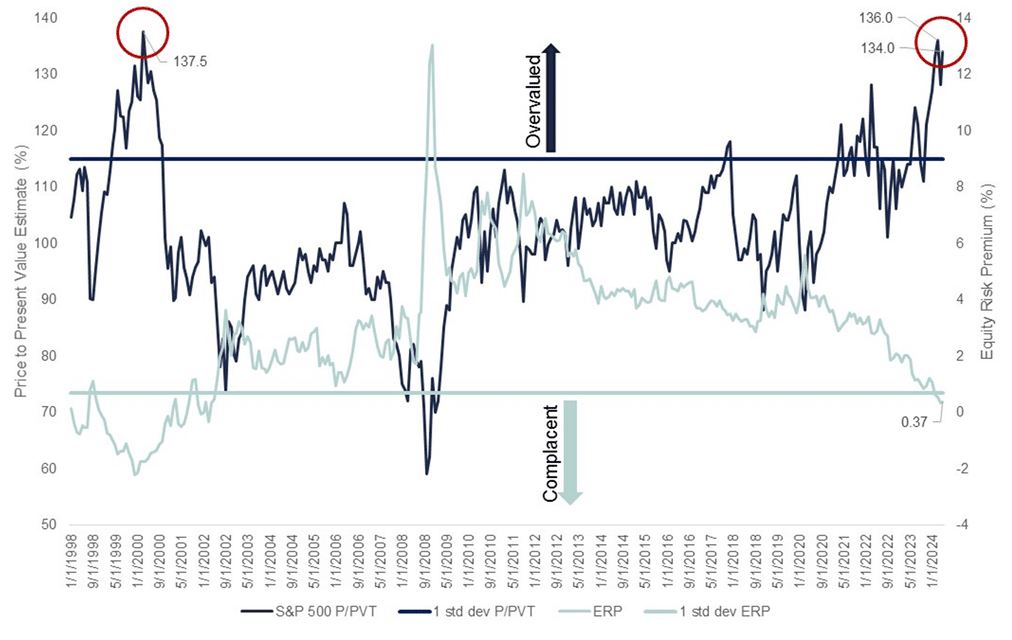

At the time, the S&P 500 was trading at 21x forward earnings (19% higher than its ten year average), implying an equity risk premium of just 54 basis points. Our proprietary calculation of price-to-present value for the market was 136%, higher than any other time outside the late 1990’s technology bubble.

As we anticipated, we experienced market volatility during April. The S&P 500 declined 5.5% from March 28th through April 19th, and on our price to present value work, was still valued at 128%. The S&P 500 subsequently climbed to a new all time high on May 21, rallying back to 135% of it’s price to present value estimate.

By the end of May, the S&P 500’s forward price to earnings ratio was at 20.6x, and our calculation of price to present value was 134% (still higher than any other time outside the late 1990’s technology bubble), with an equity risk premium of .37 (meaningfully lower than the end of March).

The set up for the equity market still does not look favorable given that stocks are overbought, valuations are rich, sentiment is overly bullish, the CBOE Volatility Index (VIX) and credit spreads are closer to lows, and the yield curve is still inverted. The only thing missing for a market set-back is a catalyst to drive earnings estimates lower. Thus, in our view, the market remains especially vulnerable to any unexpected exogenous shock.